[0:06]In this video, I will be focusing on prices, the price, because you are a trader, you are interested in prices, buy price, sell price.

[0:18]So, you need to distinguish between three main prices.

[0:24]We have two proposed prices, the bid quote, the bid price, or simply the bid.

[0:32]The ask quote, the ask price, or simply the ask. So those are simply two proposed prices.

[0:41]The sale price is an observed price, an effective price, an actual price.

[0:48]This is actually the price of the last transaction.

[0:55]The bid is the highest price a seller or a buyer is willing to pay.

[1:04]This is a cap, don't pay more than 50 dollars. This is my bid.

[1:10]The ask, the lowest price a seller is willing to accept. So this is a threshold, a minimum price.

[1:21]Don't accept less than that price, than 50 dollars. So, the bid and the ask reflect the negotiation process, the virtual, because don't forget that we're talking about an automated trading system. So the negotiation are sort of virtual negotiation.

[1:38]There is no direct contact between buyers and sellers, there is a sort of contact through the electronic order book. We'll try to explain that in our next chapters.

[1:49]So, the ask, the lowest price a seller is willing to accept. The last sell price, the sale price, this is the the price of the last transaction.

[1:58]So, the the transaction is supposed to be in, the transaction, excuse me, actually occurred.

[2:11]Make or take? Trader, the first, the basic decision that you have to make, how to buy?

[2:23]Portfolio management is about determining what to buy, the structure of your portfolio.

[2:29]This is a strategic decision, you can play the structure of your portfolio and the way you intend to make your profit in the future.

[2:39]Take, make or take, is an operational decision, how to buy.

[2:44]I can buy security, or I can sell security. So how to buy, how to sell, how to execute your transaction.

[2:53]I can make my own price, or I can take my best available price.

[2:59]If I am price taker, that situation supposed that I have some liquidity constraint.

[3:06]I need to buy, or I need to sell as soon as possible.

[3:12]I need to buy, to sell in order to get the the necessary cash that I am looking for.

[3:18]So I have some cash constraint, I need to cash out a part of my portfolio.

[3:26]And also, I need to immediately sell in order to cover my, or simply to buy in order to cover my short position.

[3:38]This is a sort of situation in which, in that sort of situation, I am obliged to execute the transaction as soon as possible, so I'm not in a good position to make my own price.

[3:51]I need in this case to take the best available price in the market. I am price taker.

[3:59]If you choose to be a price taker, or if you, or if you are obliged to be a price taker, you can execute your transaction as soon as possible immediately, but you would be, you will be obliged to accept someone else's price.

[4:14]No, making the price means simply that you will propose your own price.

[4:20]You will propose your bid if you are buyer, you will propose your ask if you are seller, so this is your price requirement, this is your price condition.

[4:28]And you cannot accept to execute the transaction at the prices that is unfavorable prices compared to what you propose.

[4:36]So that's why you need to await the arrival of someone who will accept to trade with you, who will accept your price.

[4:45]This is the downside of such a decision.

[4:49]But in the same time, you can get a better price than what is really proposed in the market.

[4:57]The starting point of any trader is that decision, make the price or take the price.

[5:04]Let's talk about liquidity, another important element of the last element that you need to understand is the concept of liquidity.

[5:13]Liquidity, it's about trading easily.

[5:18]Quickly, the speed and also how easy the trading is, will define the liquidity of the stock or the liquidity of any other security.

[5:28]When you can sell or buy that security in favorable condition in term of prices, and when you can find the counterpart in your transaction, the seller if you are buyer or the buyer if you are seller, without any problem as soon as possible, the stock is liquid.

[5:48]This is the concept of liquidity, but at the theoretical side, we will simply distinguish between four characteristics or four features of liquidity.

[5:59]Immediacy, tightness, depth, and resiliency.

[6:08]So, let's start with immediacy, immediacy is the ability to trade, the ability to trade quickly.

[6:16]And the automated trading system, especially the continuous trading system, can will allow you to trade quickly.

[6:26]They improve the speed, the pace of trading in the market.

[6:31]That's why today's markets where we can use the automated trading system to trade, to introduce our order and to process the order, are characterized by their high immediacy.

[6:43]Over-the-counter markets that might require the trader to contact many dealers before getting his order executed are characterized by their low immediacy.

[6:55]What is an over-the-counter market?

[6:58]Please, try to understand the difference between an automated trading system based on an order-driven market, and a price-driven market.

[7:13]In an order-driven market, like the example of the Casablanca Stock Exchange, and the likes of that market, all the trading process will flow through an electronic order book.

[7:25]So the orders are centralized.

[7:28]You can introduce your order, that order will be conveyed by your broker through your broker to the market, and finally the order will be entered by the the trading system in the electronic order book, and all the orders from all the cities, from all the countries will be simply added to the electronic order book where there is that interaction between buy orders and sell orders.

[7:56]Here, we talk about an over an order-driven market.

[8:00]Price-driven market, like the example of the bonds market.

[8:06]Like another, the example of the negotiable debt securities. In that such kind of markets, there is no automated trading system.

[8:16]We have key player in that markets, called the dealers.

[8:20]The dealers are those players who are present in the bond market and negotiable debt securities markets, they make the market.

[8:31]If you are buyer, there will be sellers. If you are sellers, there will be buyers. So any transaction would be executed against the dealers.

[8:42]It means simply that we are in the sort of decentralized markets, why?

[8:46]Because there is no central price where dealers, where we can find that dealers.

[8:52]No, simply that trading process will be processed through the the verbal negotiation, through by using the phone.

[9:00]If I want to sell or buy bonds or negotiable debt securities, or maybe buys and sells currencies in the the stock in the foreign exchange markets, for the case of Morocco, I need to contact many dealers by phone, proposed my prices and try of course to receive their proposals in order to execute the transaction.

[9:23]So, over-the-counter markets, which are simply a sort of price-driven markets, where the key players are the dealers, are characterized by their low immediacy.

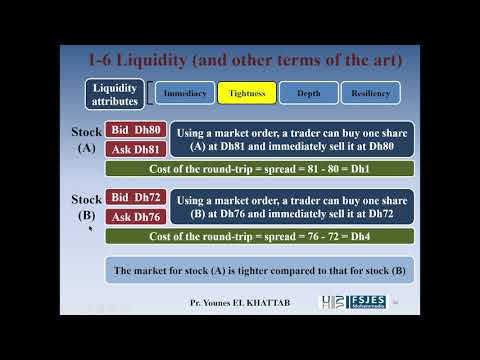

[9:32]Tightness, tightness is the tightness of the bed of the spread.

[9:51]The spread, this is a sort of transaction cost proxy variable.

[9:57]Why? Because when we have a large spread, it means that we have a high transaction cost.

[10:05]When we have a low spread, it means simply that we have a low transaction cost.

[10:11]Why do we consider that a transaction cost? So considering a round-trip purchase and sale.

[10:18]Let's say that we use a market order that is taken the best available price in the market to buy security to buy stock and sell it immediately.

[10:29]So suppose that first the first operation is a buy, buy transaction.

[10:34]I will simply buy that securities, that securities at the ask price, which is the best available ask price in the market.

[10:45]Suppose that I need to buy the security or the stock A, I will buy the stock A in this case at 81 dirhams.

[10:53]And immediately sell that stock at 80 dirhams. So the the cost of this round trip is 80 minus 81 equals minus 1.

[11:04]So I have a loss of one dirham.

[11:07]Let's execute the same transaction for the stock B.

[11:11]For the stock B, market in stock B is 76 dirhams ask or 72 dirhams bid and the ask is 76 dirhams.

[11:24]If I want to buy that stock in a sort of round-trip purchase and sale, I can buy the stock at the ask price at 76 dirhams and immediately sell the stock as at the bid price 72 dirhams.

[11:38]The cost of my transaction, of my round trip is 72 minus 76 equals 4. So here, the loss is 40 dirhams.

[11:50]or four dirhams, excuse me.

[11:53]One is less than four.

[11:57]Which means simply that market for stock A is tighter compared to that for stock B.

[12:06]And transaction cost in market in stock market for the stock A are lower than those for the for the market of the stock B.

[12:15]Let's imagine simply that we have the buy side and sell side.

[12:21]And we have the spread. The spread is the difference between the best available ask in the market and the best available bid in the market.

[12:33]At the buy side, there is a sort of competition between the potential buyers in order to propose the best prices from the sellers' point of view.

[12:45]And if we have really that sort of hard competition between them, the result will be a an increase in the bid.

[12:53]Because the best prices from the sellers' point of view are the highest prices, which means simply that competition between the buyers at the buy side will lead to an increase in the ask, so in the increase in the prices proposed by the seller, which are simply the ask.

[13:27]When we have a decrease in the ask, an increase in the bid, it means simply that the gap between the two proposed prices will decrease and the market will be tighter.

[13:37]So this is and the spread will decrease and the market will be tighter. This is what we call tightness.

[13:47]Markets liquidity, the liquid markets are characterized by their tightness.

[13:55]They are tighter compared to the illiquid markets.

[14:00]Depth, this is the third feature or the third characteristic of liquidity.

[14:12]Liquid market are characterized by the presence of a fair amount, substantial amount of orders at the buy side and the sell side.

[14:20]When the market is liquid, the potential share, the potential buy orders, potential sell orders, the quantities that correspond to those orders are substantial and important quantity, like what we have for the stock A, that here what we have is 80 dirhams bid for 50,000 shares and 10,000 shares offered at 81 dirhams offered at 81.

[14:36]So, you have the substantial quantity of 5,000 shares at the buy side, that is the demand, and substantial quantity of 10,000 shares, that is the supply, which means that market is really a deep market.

[14:58]Compared to the stock B, where you have only one shares at the buy side, 100 shares at the buy side and 100 shares at the ask side.

[15:09]Keep in your mind, please, tightness is about the difference between the ask and bid, so it's about the spread.

[15:16]The lower the spread, the tighter is the market. The depth is about the quantities present at the buy side of the electronic electronic order book and the sell side of that book.

[15:30]If you have a substantial quantity, the market is deep.

[15:35]The more substantial, the more important the volume in the two sides of the electronic order book, the deeper the market is.

[15:44]This is how can I describe that important feature, which is the depth.

[15:50]Finally, resiliency, in terms of bounce back, any price changes that may might accompany the large trade are quickly short-lived and quickly dissipate.

[16:03]So if there is a shock, came from whatever the the reason of that shock, here, we take the example of a large trade.

[16:11]Large trade have an immediate a result immediate or precaution on prices.

[16:19]An increase, an important buy orders, the result will lead simply to a an increase in the prices.

[16:30]And an important sell order will lead to a decrease in the prices. So this is a sort of disturbance price prices of prices.

[16:39]A shock that will have an impact on prices, but if the market is resilient, those prices will get back their initial level, their steady state level, their long-term level as soon as possible, immediately, which means simply that the market is resilient.

[16:55]Resiliency is the fourth feature of liquidity. So, that attribute, it's so important.

[17:03]Because why? If there is some reasons at the market level, or at the eco economic level, or or at the macroeconomic level, at the microeconomic level, or simply at the market level.

[17:14]Those shocks will simply disturb the prices, will lead to simply a sort of gap between the price and the long-term trend of that price, the long-term level of the of that price.

[17:27]If the market is resilience, those short-term disturbances will simply disappear, dissipate and prices will get back their initial level in a short period.

[17:39]That's why I describe that as price changes that might accompany shocks or large trade are simply short-lived and quickly dissipate.